CGEPHIS Health Scheme 2025: In a landmark move to improve healthcare accessibility and security, the Central Government has launched a new initiative titled the Central Government Employees and Pensioners Health Insurance Scheme (CGEPHIS). This scheme is poised to replace the long-standing Central Government Health Scheme (CGHS) and is designed to deliver broader, more modern, and inclusive medical coverage for government employees and retirees.

Let us find out what CGEPHIS is, how it is different from CGHS, who will benefit from it, and what it means for the future of healthcare among central government employees and pensioners.

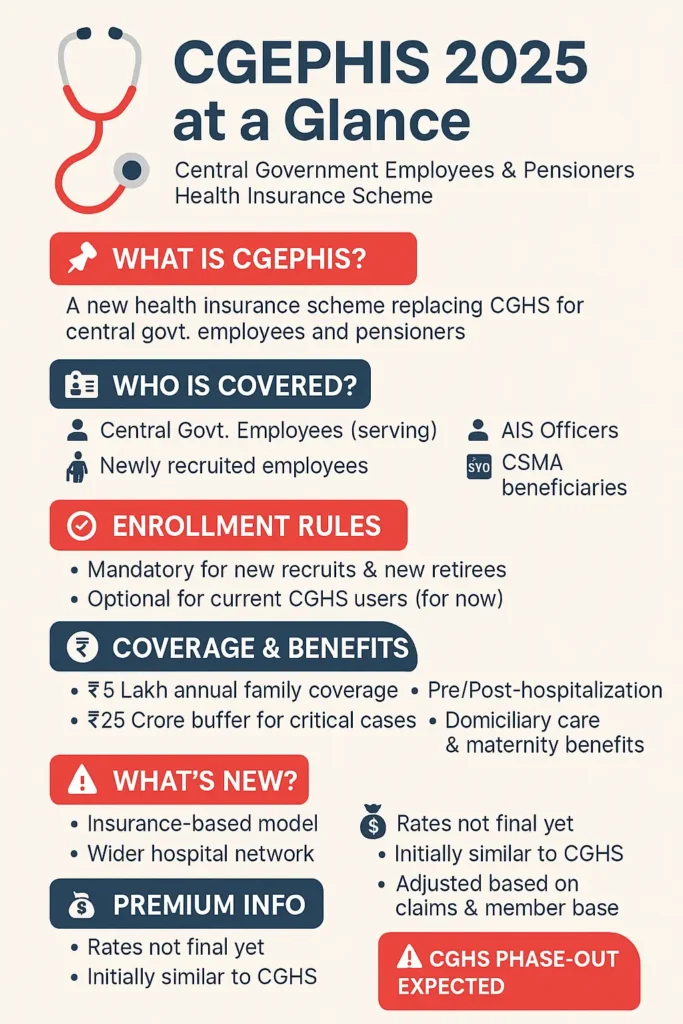

What is CGEPHIS?

As defined by CGEPHIS, central government employees and pensioners health insurance scheme. An amalgamation of 21 health schemes, it seeks to fundamentally transform access to medical care for central government employees and pensioners. Unlike CGHS, which is based on fixed facilities, CGEPHIS uses a health insurance model, which has wider reach and provides flexibility in accessing health services.

The scheme not only covers a broader range of treatments but also includes services that were previously limited or unavailable under CGHS.

Who Will Benefit from CGEPHIS?

The new scheme covers a large pool of beneficiaries, including.

- Serving Central Government employees.

- Retired government pensioners.

- All India Services (AIS) officers.

- Newly recruited central government staff.

- Individuals currently covered under Central Services (Medical Attendance) Rules (CSMA).

This transition is expected to impact over 17 lakh serving employees and nearly 7 lakh pensioners, underlining the wide-scale influence of CGEPHIS.

Mandatory Enrollment vs. Voluntary Opt-In

One of the significant changes under CGEPHIS is the enrollment requirement. Here’s how it works.

- Mandatory for New Recruits and Retirees: All new employees joining central government services, and those retiring after the launch of CGEPHIS, will be required to enroll in the scheme.

- Optional for Existing Beneficiaries: Current CGHS members (both employees and pensioners) can choose to opt into CGEPHIS voluntarily. However, this flexibility may be short-lived, as the government has indicated a gradual phase-out of the CGHS.

This dual-enrollment model allows time for adjustment while encouraging long-term standardization under a single, more efficient health insurance scheme.

What Does CGEPHIS Cover?

The scope of medical coverage under CGEPHIS is one of its biggest advantages. It includes:

- Treatment of Pre-existing Conditions: No exclusions for existing diseases.

- Pre and Post-Hospitalization: Expenses incurred before and after hospital stays are covered.

- Domiciliary Hospitalization: Treatments at home that would otherwise require hospitalization.

- Daycare Procedures: Coverage for procedures that do not require overnight hospital stays.

- Maternity and Newborn Benefits: Care for mothers and infants is included under the plan.

This extensive coverage ensures that beneficiaries get not only emergency treatment but also long-term care and family-oriented medical support.

Health Insurance Coverage and Limit

The CGEPHIS introduces a structured insurance model with clear financial boundaries:

- Annual Coverage Limit: Up to ₹5 lakh per annum per family unit, inclusive of the employee or pensioner and their dependents.

- Additional Buffer (Corporate Sum Insured): In cases where treatment costs exceed ₹5 lakh, an additional corporate buffer of up to ₹25 crore will be available for critical or high-value claims. However, this buffer will be accessible under higher premium slabs or special conditions.

Premium Structure: Still Evolving

While CGEPHIS has been formally introduced, its premium structure is still under development. Currently:

- It is expected to be in line with existing CGHS contributions to start with.

- The premium may be revised in the future based on claim volumes, the number of members enrolled, and fund sustainability.

- Initially, around 1 lakh employees and pensioners are expected to enroll to determine a more accurate premium estimate.

Since the exact contribution amount is still pending, it’s important for potential beneficiaries to stay updated through official announcements.

Key Differences Between CGHS and CGEPHIS

| Feature | CGHS | CGEPHIS |

|---|---|---|

| Coverage Type | Facility-based care through empanelled hospitals | Health insurance model with broader network |

| Enrollment | Voluntary (mostly) | Mandatory for new entrants and retirees |

| Coverage Limit | No monetary cap, limited to CGHS empanelled services | ₹5 lakh per year per family + buffer |

| Portability | Limited to CGHS cities | Nationwide access through insurance tie-ups |

| Cashless Treatment | Only in CGHS facilities | Widely available in network hospitals |

| Pre/Post Hospitalization | Limited coverage | Full inclusion |

Why is CGEPHIS Important?

The introduction of CGEPHIS marks a significant transformation in the healthcare delivery system for government employees.

- Broader Accessibility: The insurance-based model ensures treatment is not limited to CGHS cities.

- Modern Healthcare Practices: Includes daycare surgeries, critical care, and advanced treatments.

- Financial Protection: With a defined annual limit and buffer coverage, beneficiaries are protected from large medical expenses.

- Uniform Coverage: A unified scheme for all future employees helps in better management and tracking of healthcare needs.

What Should Employees and Pensioners Do?

As the scheme gradually rolls out, here are steps current and future government employees should consider.

- Stay Informed: Follow updates from the Ministry of Health & Family Welfare regarding enrollment deadlines and premium details.

- Review Options: If you’re an existing CGHS beneficiary, compare benefits and make an informed choice whether to opt into CGEPHIS.

- Consult HR or Departmental Offices: Departments will have dedicated personnel to assist with the transition process.

- Prepare Documentation: Get your and your dependents’ medical records and identification ready for smooth enrollment.

Conclusion

The Central Government Employees and Pensioners Health Insurance Scheme (CGEPHIS) is a step towards modernising healthcare for India’s public sector employees. By offering structured coverage, modern health benefits and a scalable insurance model, the scheme ensures better protection, improved care and streamlined services.

Like any new policy, the success of CGEPHIS will depend on effective implementation and active participation of stakeholders. For government employees and pensioners, this is a crucial moment to understand their healthcare rights and make informed choices for themselves and their families.